Welcome back, hermanos!

For many of us, owning a home is the ultimate symbol of stability and building wealth for our families. As young Latinos navigating our professional lives and managing money in the U.S., we know that the path to homeownership often feels complex. One of the biggest hurdles? The credit score.

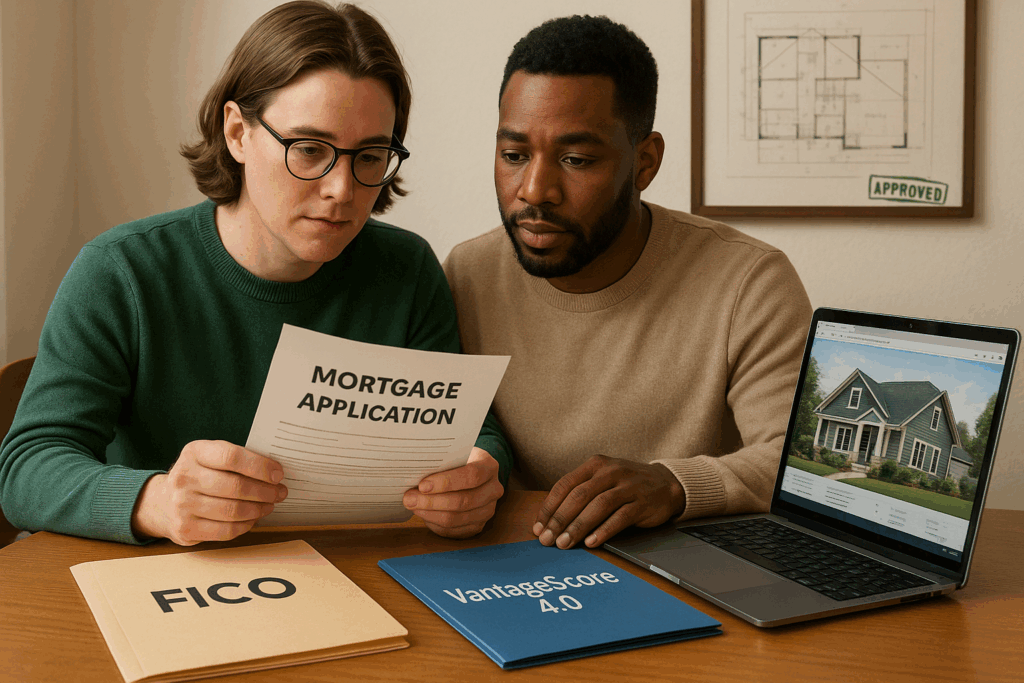

For decades, the FICO score has been the gatekeeper for mortgage loans, especially those backed by government-sponsored entities like Fannie Mae and Freddie Mac. But a major shift is underway that could make the dream of getting those keys a reality for more of our community.

The Credit Score Evolution: A Game Changer

The Federal Housing Finance Agency (FHFA) recently approved an important update: lenders underwriting mortgages backed by Fannie Mae or Freddie Mac now have a choice between two major credit score models:

- FICO: The long-established industry standard.

- VantageScore 4.0: A newer, more inclusive model.

This is a significant change because it injects choice into a system previously dominated by a single standard. It’s not about one score replacing another; it’s about acknowledging that a person’s financial reliability can be measured in multiple, equally valid ways.

Why This Matters Deeply for the Latino Community

This shift is particularly relevant for Latino aspiring homeowners. Why? Because the VantageScore 4.0 model is designed to consider what’s called “alternative data.” This includes financial behaviors that often don’t show up on traditional credit reports, such as:

- Regular, on-time rental payments.

- Consistent utility and phone bill payments.

For many new professionals, recent arrivals, or those starting without a long history of credit cards and loans, these alternative payments are the true reflection of financial responsibility.

Considering alternative data is key to unlocking homeownership for historically underserved groups. For instance, while Latinos have made massive strides in economic power (driving significant GDP growth) we still face disparities in wealth accumulation. According to the latest data, the homeownership rate for the Hispanic community in the U.S. is $49.5, a figure we are determined to grow as a community (“Quarterly Homeownership Rates by Race and Ethnicity of Householder: 1994 to Present (Table 16)”). The inclusion of VantageScore 4.0 provides a more flexible and comprehensive path to qualify, potentially boosting that homeownership rate by accurately reflecting our consistent payment behaviors.

FICO is Still a Force

It’s important to be clear: FICO is not disappearing. Its legacy, reliability, and strong history mean that many mortgage lenders will continue to rely on it. Transitioning an entire industry to a new score takes time and effort. As a result:

- Maintain Your Score: You still need to manage your finances responsibly to ensure a healthy score with both FICO and VantageScore.

- Lender Choice: Lenders can now choose which score to use, meaning you might still encounter the FICO model depending on where you apply.

The bottom line is that the more ways you have to demonstrate creditworthiness, the better your opportunities are.

What This Means for Our Financial Future

As we build our professional lives and manage our finances, this scoring change offers important benefits:

- Greater Access: If you have been responsibly paying rent and utility bills for years but lacked a substantial credit card history, the new model offers a stronger chance to qualify for a good mortgage rate.

- Flexibility: We now have more ways to prove to a lender that we are a low risk, even if our credit journey looks different from the traditional path.

- Better Terms: Competition between scoring models and between lenders can lead to better interest rates and fewer fees for us, the borrowers.

We are a community known for our work ethic and financial resilience. This shift in credit scoring is an official step toward recognizing that resilience in a way that truly matters: by making homeownership more accessible. It’s a powerful move that helps us convert our strong financial behaviors into stable, generational wealth.

Keep learning, keep saving, and keep managing your finances wisely. We’re in this journey together!

👉 Ask Gabi anything, anytime.

Stay tuned! We got you!

GabrielTeam