As the rhythm of fall takes over (maybe it’s a new city, a new job, or just a new semester) it’s time for a critical financial check-in. For young professionals and students in the U.S., few financial issues are as complex or as significant as student loans. We know this journey hits our community differently.

We are often driven by a goal greater than just ourselves, and that mission can come with a higher financial burden. For instance, Hispanic and Latino borrowers are the most likely to delay major life milestones, like getting married (32.5%) or having children (37.4%), specifically due to their student loan debt (Education Data Initiative).

We’ve worked too hard to let this debt stall our future. With major federal program shifts happening, this fall is the perfect moment to take a sharp, proactive look at your loans. This is about protecting our hard-earned progress and securing the future we deserve.

Here are four essential moves to make regarding your student loans this season:

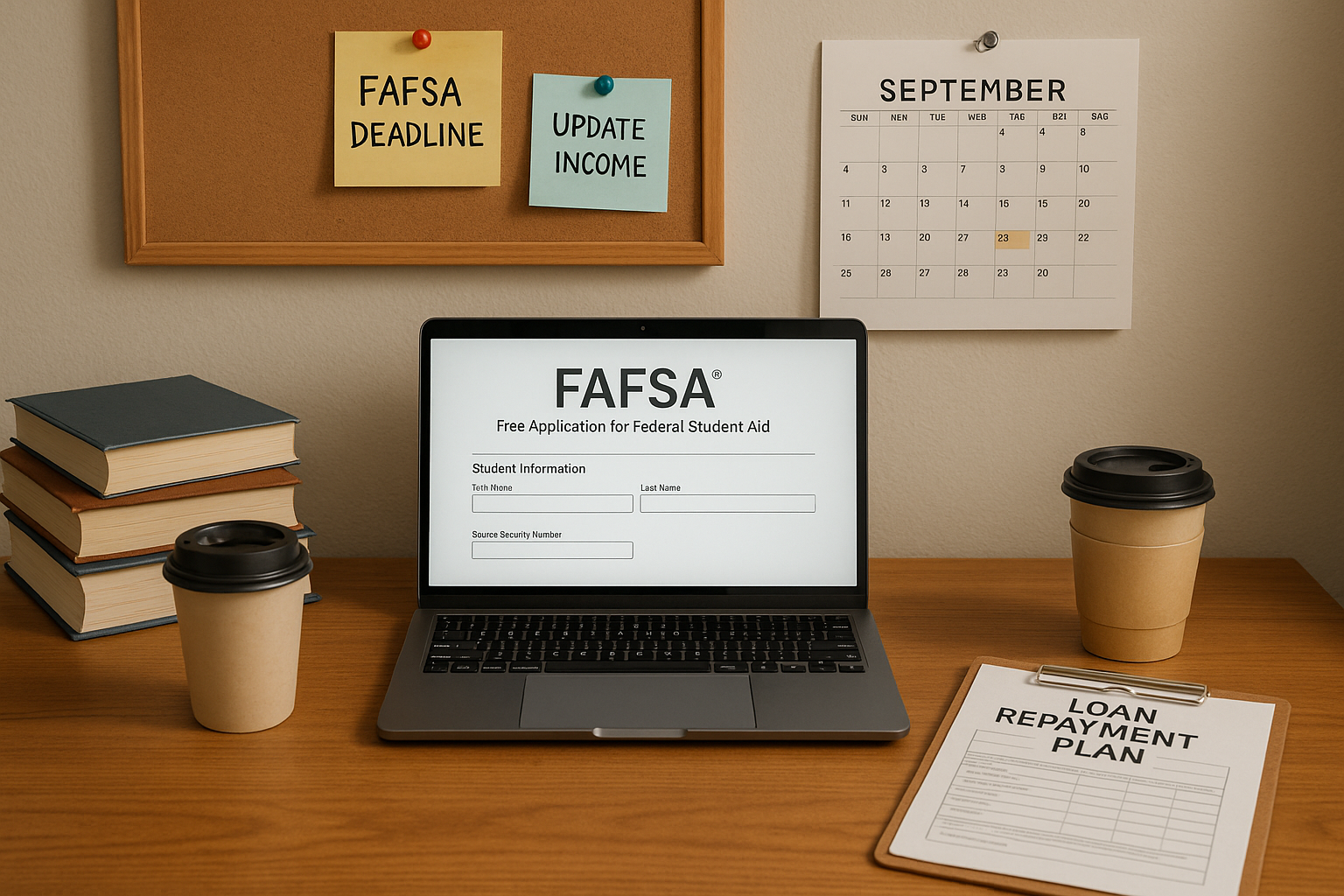

1. Get Ahead of the FAFSA Filing Rush

The Free Application for Federal Student Aid (FAFSA) is the critical first step for federal grants, work-study, scholarships, and loans. Many of us are balancing school, family, and work, so maximizing aid is essential.

- File Early: While the federal deadline for the 2025–26 school year is June 30, 2026, many states and individual colleges have deadlines much earlier, sometimes as soon as October or November. These institutions often award aid on a first-come, first-served basis. By delaying, you risk missing out on grants, which is free money you don’t have to repay.

- The Latest FAFSA: The application underwent a significant overhaul to simplify the process. Get familiar with the changes now to avoid surprises and ensure an accurate, timely submission.

2. Update Your Income for Income-Driven Repayment (IDR) Plans

If you are currently on an Income-Driven Repayment (IDR) plan, like the popular SAVE Plan, your monthly payment is calculated based on your reported income and family size. Your income can change quickly as you transition from college student to working professional, and keeping the government updated is non-negotiable.

- Avoid Inflated Payments: If you don’t recertify your income and family size annually, your payments could jump to the higher, non-IDR level, which is a budget shock no one needs.

- Automatic Verification is Your Friend: Use the IRS Data Retrieval Tool when you recertify. Better yet, opt into automatic annual verification. This ensures your payment is always based on the most current, lowest possible number, keeping more money in your pocket for rent, savings, or investments.

3. Face the Interest: Don’t Let it Pile Up Quietly

Even if your federal loan payments were deferred, for example, during a forbearance period or while you are still enrolled in school, interest is likely accumulating and adding to your total debt.

- The Power of Interest: Student loan balances grew significantly for many borrowers, even when payments were paused. For borrowers on the SAVE plan, unpaid monthly interest might not be added to your principal balance, but it’s still good practice to chip away at what you can.

- Strategy: If your budget allows, make interest-only payments now. This is a small, smart defensive financial move that prevents your total debt from ballooning over time.

4. Understand Future Program Changes

The federal student loan landscape is constantly shifting, and staying informed is how we stay empowered. You need to know which plans are changing or ending so you can make the best choice for your long-term finances.

- Know Your Plan’s Status: The existing IDR options (like IBR, PAYE, and ICR) will continue to be available to current borrowers, but you must know the specific terms and when you may need to act.

- The New Landscape: Always check the Department of Education’s official website for the latest on new or revised repayment plans to ensure you are enrolled in the one that gives you the maximum monthly payment relief and the best path to forgiveness. The U.S. Department of Education confirms all new rules are posted there (“Repayment Plans”).

Our financial future is nuestro responsibility, and mastering student loan management is one of the most critical steps. Let’s start this season with financial clarity and confidence.

👉 Ask Gabi, the “judgment free zone” for all of your financial questions!

Stay tuned! We got you!

GabrielTeam